Compare emergency loan offers carefully before choosing the fastest approval or the smallest advertised payment. What you get, when you get it, and the total bill can really vary between lenders, even for the same loan amount.

When a bill’s urgent, it’s easy to just think about getting money fast. As a result, borrowers may not notice aspects like origination fees, quick repayment deadlines, automatic withdrawals, or a first payment date that is sooner than they had planned.

This guide explains how to compare emergency loan offers side by side, including APR, fees, net loan proceeds, payment frequency, funding time, and total repayment.

Why You Should Compare Emergency Loan Offers Carefully

It’s not just about the approved amount with an emergency loan offer. It is a complete repayment agreement that can affect several future paychecks.

One lender may offer quick funding but deduct a large fee before depositing the money. Another may take an extra business day but provide more usable funds and a lower total cost. A third may advertise a small payment while extending the debt for much longer.

Comparing offers can help you answer four important questions:

- How much money will I actually receive?

- How much will each payment be?

- How long will I be making payments?

- How much will I repay in total?

Do not choose an offer until you can answer all four.

1. Start With the Amount You Actually Need

Before comparing lenders, write down the exact cost of the emergency. You should use a repair estimate, medical bill, utility notice, or something else you trust instead of guessing.

Borrowing more than necessary can increase:

- The scheduled payment

- The amount of interest charged

- Origination fees based on a percentage of the loan

- The total repayment amount

- The time needed to repay the debt

Borrowing too little can also create a problem. The approved amount might not cover the expense completely after fee deductions.

For example, an approved $1,000 loan does not necessarily place $1,000 in your account. If the lender deducts an origination fee, the usable amount may be lower.

2. Confirm What Type of Loan Is Being Offered

People often use the phrase “emergency loan” as a general marketing term. The underlying product could be a personal installment loan, payday loan, line of credit, secured loan, or another form of borrowing.

Before comparing offers, identify:

- Whether the loan is installment-based or due in one payment

- Whether the rate is fixed or variable

- Whether collateral is required

- Whether payments are monthly, biweekly, or tied to payday

- Whether the lender can automatically withdraw payments

Do not consider two products equivalent just because both advertise for emergencies.

3. Compare the APR, Not Just the Interest Rate

The annual percentage rate, or APR, is one of the key figures used to compare borrowing costs. It is broader than the interest rate because it may reflect certain fees charged with the loan.

When reviewing APR:

- Use the APR shown in the actual offer, not just an advertised starting rate

- Confirm whether the rate stays fixed throughout the full term.

- Confirm whether the offer is final or still conditional

- Compare offers for the same loan amount and a similar repayment period

An advertisement may say rates “start at” a low percentage, but your offered APR may be higher based on the lender’s review.

The Consumer Financial Protection Bureau explains that APR measures the interest rate plus certain additional loan fees, making it useful when comparing borrowing costs.

4. List Every Fee Attached to the Offer

Fees can change the real value and cost of an emergency loan. Do not assume that two offers with similar APRs will provide the same amount of usable money.

Look for:

- Origination fees

- Application fees

- Administrative or processing fees

- Late payment fees

- Returned payment or insufficient-funds fees

- Account maintenance fees

- Prepayment penalties

- Optional products added to the loan

The lender deducts some fees before the loan reaches your account. Others apply only when a specific event occurs, such as a late or returned payment.

Ask the lender to explain any charge you do not recognize. A fee should not remain unclear simply because the expense is urgent.

5. Calculate the Net Loan Proceeds

The net loan proceeds are the amount you receive after upfront deductions.

Use this simple comparison:

Approved loan amount − upfront fees = amount received

Suppose one lender approves $1,200 and deducts a $120 origination fee. The amount deposited may be $1,080, even though the repayment obligation is based on the approved loan.

For each offer, write down:

- The approved amount

- The amount of every upfront deduction

- The exact amount expected to reach your account

Then compare the net proceeds with the emergency expense. An offer is not useful if the deposited amount is too small to solve the problem.

6. Compare the Total Repayment Amount

The total repayment amount indicates how much you should pay by the end of the loan if you make payments as scheduled.

This number may be more useful than the monthly payment alone.

A smaller payment may look attractive, but it may continue for more months. A larger payment may finish the loan sooner but create too much pressure on your budget.

Compare:

- The principal borrowed

- Total interest

- Required fees

- The number of payments

- The amount of each payment

- The final total repaid

The least expensive offer is not automatically the right choice if its payment is unaffordable. The goal is to find an offer with both a manageable schedule and a reasonable total cost.

7. Review the Payment Frequency and First Due Date

Do not assume every emergency loan uses monthly payments. Some offers may require weekly, biweekly, semimonthly, or payday-based payments.

Confirm:

- The first payment date

- How often payments are due

- The amount of each payment

- Whether the final payment is different

- Whether automatic withdrawals are required

A payment that looks small may be due every two weeks rather than once a month. Compare the frequency with your pay schedule and regular household bills.

Look at your next several paychecks, not just the current one. Make sure the loan payment will not cause you to miss rent, utilities, food, insurance, or any other essential expense.

8. Compare Funding Speed Carefully

Funding speed matters during a real emergency, but the wording used by lenders can be easy to misunderstand.

Separate these stages:

- Application review

- Preliminary decision

- Final approval

- Loan agreement acceptance

- Funds sent by the lender

- Funds posted by your bank

“Same-day decision” does not necessarily mean same-day approval. “Same-day funding” may mean the lender sends the money that day, not that your bank makes it immediately available.

Application cutoff times, additional verification, weekends, holidays, and bank processing can also affect funding.

Read what borrowers should know about same-day emergency loans before relying on a specific funding timeline.

9. Check Whether the Offer Is Final or Conditional

A pre-qualified or preliminary offer may change after the lender verifies your information.

Before treating an offer as final, ask:

- Has my identity been verified?

- Has my income been confirmed?

- Has the lender completed its credit review?

- Can the APR or loan amount still change?

- Are additional documents required?

Prequalification can be useful for comparison, but it is not the same as final approval.

Also ask whether checking the offer uses a soft or hard credit inquiry. A hard inquiry may appear on your credit report, while a soft inquiry rarely affects your credit score.

10. Review Early Payoff and Late Payment Rules

Your financial situation may change during the loan term. Review what happens if you pay early or miss a scheduled payment.

Check:

- Whether there is a prepayment penalty

- How extra payments are applied

- Whether interest is recalculated after early payoff

- The amount of any late fee

- Whether a grace period applies

- What happens after a returned automatic payment

- Whether missed payments may be reported to credit bureaus

Be aware that an additional payment may not decrease the principal. Confirm how the lender applies additional funds.

11. Compare Secured and Unsecured Offers Carefully

Some emergency loan offers may require collateral. A secured offer might use a vehicle, savings account, or another asset to support the loan.

A secured loan may have different pricing or approval standards, but it also creates a direct risk to the pledged asset if the loan is not repaid.

Before accepting a secured offer, understand:

- Which asset secures the loan

- What rights the lender has after missed payments

- Whether additional filing or lien fees apply

- How the collateral will be released after repayment

Do not pledge an essential asset without understanding the consequences.

12. Use a Side-by-Side Comparison Table

A written table makes it easier to see differences that may be missed when switching between lender websites.

Fill in the table using the written disclosures from each lender. Do not rely on advertisements or verbal eexplanations

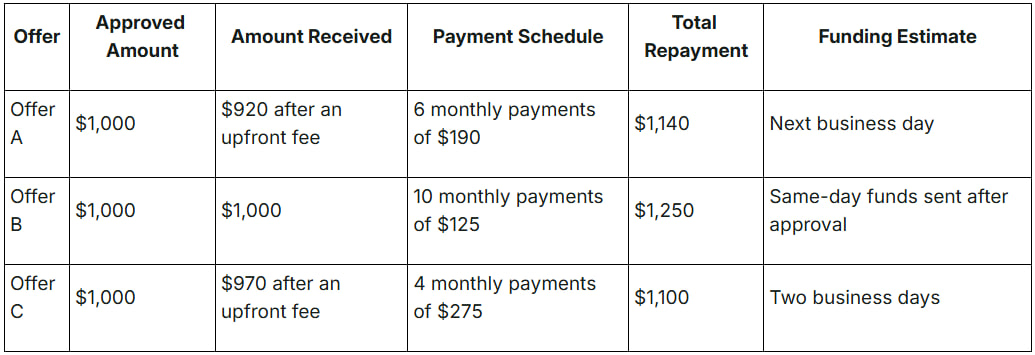

Illustrative

The following example simplifies the situation and aims only to show how offers can differ.

Offer B has the smallest monthly payment and the fastest advertised funding, but it also has the highest total repayment in this example. Offer C has the lowest total repayment, but its payment is much higher.

The correct choice would depend on the actual disclosures, the urgency of the expense, and whether the borrower can safely afford the scheduled payment.

13. Verify the Lender Before Sharing Information

Emergency loan applications may request sensitive personal and financial details. Make sure it’s a legit company before giving them your SSN, bank details, or ID.

Look for:

- A clear legal business name

- Customer service contact information

- A physical or mailing address

- Required state licensing or registration information

- A secure website connection

- Written loan terms before acceptance

Be cautious if someone contacts you unexpectedly and asks for payment before providing the loan.

The Federal Trade Commission warns that advance-fee loan scams may promise access to credit while requiring money upfront.

14. Watch for Emergency Loan Red Flags

Slow down when an offer includes:

- Guaranteed approval

- No review of income or repayment ability

- An upfront payment is required before funding

- Requests for gift cards, cryptocurrency, or wire transfers

- Pressure to accept immediately

- No written explanation of the APR or fees

- A loan agreement that cannot be reviewed in advance

- Terms that change after you provide personal information

A legitimate offer should clearly explain how much you will receive, what you must pay, and when each payment is due.

15. Consider Lower-Cost Alternatives Before Accepting

Comparing loan offers should also include comparing the loan with non-loan options.

Depending on the expense, you may be able to use:

- A payment extension from the biller

- A medical or utility payment plan

- Part of an emergency fund

- A credit union small-dollar loan

- An employer pay advance

- Local community assistance

- A smaller temporary loan from family or friends

Read our guide to seven emergency loan alternatives that may cost less before taking on new debt.

Borrowers with weaker credit can also review what to know before applying for emergency loans with bad credit.

Questions to Ask Before Accepting an Offer

- Is this the final approved offer?

- What is the APR?

- Is the rate fixed or variable?

- Which fees does the system deduct before funding?

- How much money will reach my account?

- What is the payment amount and frequency?

- When is the first payment due?

- How many payments are required?

- What is the total repayment amount?

- What happens if a payment is late or returned?

- Can I repay early without a penalty?

- When will the lender send the money?

- Could my bank delay access to the funds?

- Is collateral required?

Emergency Loan Offer Comparison Checklist

Before choosing a lender, confirm that you have compared:

- The same requested amount across offers

- The actual APR offered to you

- All upfront and potential fees

- The amount deposited after deductions

- The payment amount and frequency

- The first payment date

- The full repayment period

- The total repayment amount

- The expected funding timeline

- Early payoff and late payment rules

- Any collateral requirement

- The lender’s identity and contact information

- Lower-cost alternatives

Choose Based on the Full Offer, Not One Attractive Number

Learning how to compare emergency loan offers can help you avoid choosing a loan based only on speed, a low advertised rate, or a small payment.

Start with the amount you truly need. Then compare the APR, fees, net proceeds, payment schedule, total repayment, and realistic funding time.

The strongest offer is not necessarily the one that arrives fastest. It is the one that provides enough money for the emergency, clearly explains the cost, and fits your budget without creating another financial problem.

{kind=link}