Knowing how to compare personal loan offers can help you look beyond the lowest monthly payment and understand the real cost of borrowing. A loan offer may look affordable at first, but the full cost depends on the APR, fees, repayment term, total repayment amount, and lender rules.

A personal loan may seem straightforward at first. You borrow a set amount of money, repay it over time, and make monthly payments until you pay off the balance.

The harder part is comparing offers. Two loans can have the same loan amount but very different overall costs. One may have a lower monthly payment but a longer repayment term. Another may have a higher monthly payment but cost less overall. Some lenders charge fees upfront, while others do not. That is why comparing personal loans is not only about finding the lowest payment.

This guide explains how to compare personal loan offers by looking at the full cost, not just the payment shown in an advertisement.

Before you apply, it helps to understand what affects the real cost of a loan: APR, fees, repayment term, rate type, collateral, and early payoff rules.

Start With the Total Cost, Not Just the Monthly Payment

Many people look at the monthly payment first. That makes sense because the payment has to fit into your budget. But the payment alone does not show the full cost.

Sometimes, a lower payment simply means the loan lasts longer. That may make the payment easier to handle month to month, but it can also increase the total amount of interest paid over the life of the loan.

For example, a shorter loan term may come with a higher monthly payment, but you may pay less interest overall. You can lower your monthly payment with a longer term, but you might pay more interest when the loan is fully repaid.

When comparing personal loans, look at both numbers:

- The monthly payment

- The total amount you will repay

If a lender provides a repayment schedule or an estimated total repayment amount, review it closely. It can show whether the lower monthly payment is actually saving money or simply extending the loan.

Know the Difference Between Secured and Unsecured Loans

Lenders may offer personal loans that are secured or unsecured.

An unsecured personal loan does not require collateral. The lender reviews your financial profile, such as credit history, income, debt level, and other eligibility factors. Many personal loans are unsecured, especially loans used for general expenses, debt consolidation, or unexpected bills.

A secured personal loan requires collateral. Collateral is something of value that backs the loan. Depending on the lender and loan type, collateral could be a vehicle, a savings account, or another asset. Because collateral can reduce lender risk, a secured loan may sometimes offer a lower rate or a higher loan amount.

But secured loans also carry more risk for the borrower. If you do not repay the loan as agreed, the lender may have rights related to the collateral under the loan agreement.

That does not mean secured loans are always bad or unsecured loans are always better. It means you need to understand the trade-off. A lower interest rate is useful only if the loan fits your budget and you are comfortable with the potential risk.

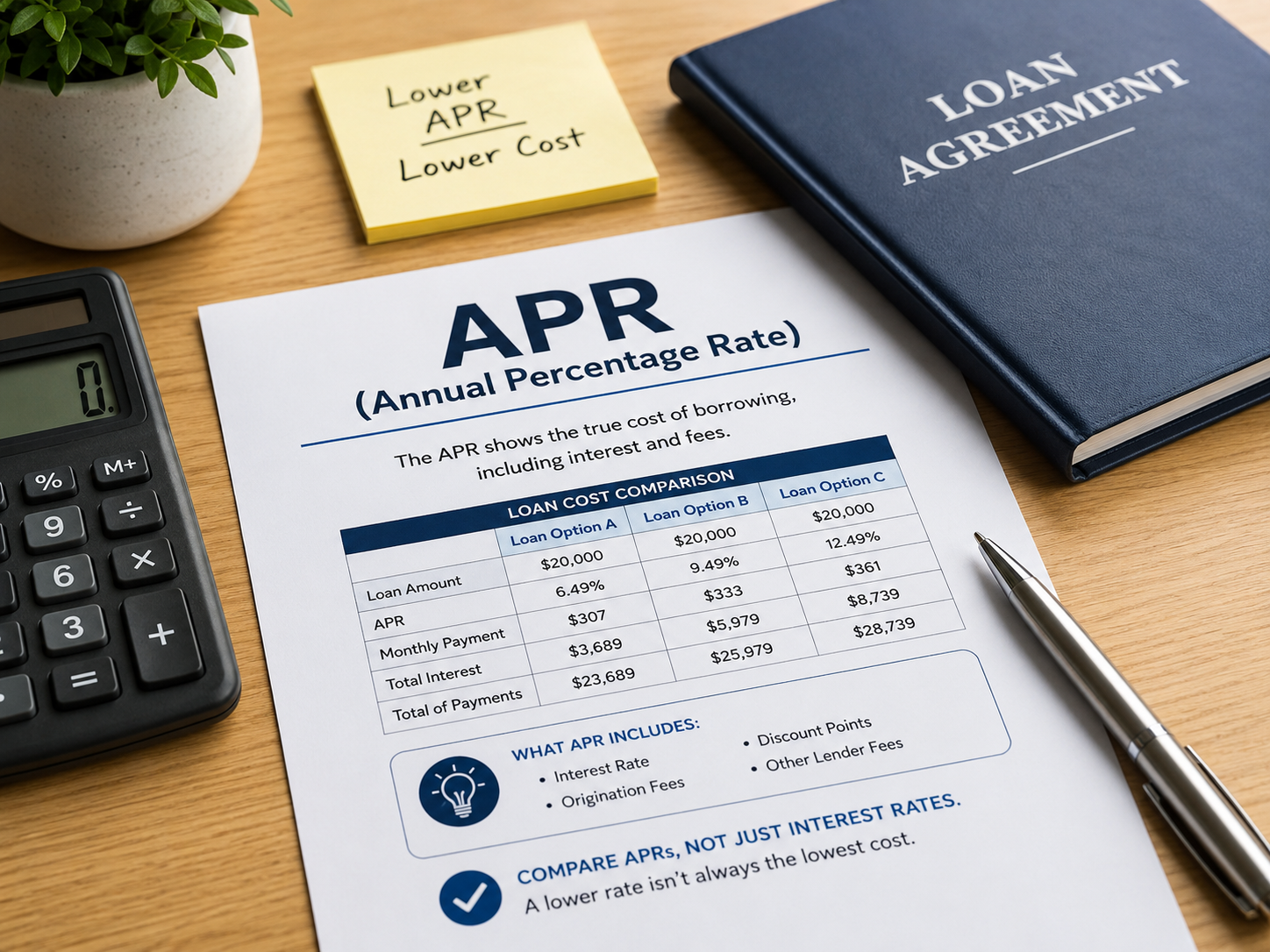

How to Compare Personal Loan Offers by Looking at APR

The interest rate is important, but APR is often more useful when comparing loans.

APR stands for annual percentage rate. It gives a broader view of the yearly cost of borrowing because it may include the interest rate and certain required fees. A loan with a low advertised rate may not always be the cheapest option if it includes high fees.

When reviewing APR, pay attention to whether the lender is showing:

- A starting APR

- A representative APR

- A range of possible APRs

- The actual APR offered to you after review

The rate you qualify for may depend on your credit history, income, loan amount, repayment term, and the lender’s approval criteria.

This is one area where many borrowers get confused. A lender may advertise a very attractive rate, but your final offer could be different. The final offer matters.

A Longer Repayment Term Can Make a Loan Appear Less Expensive

Loan term matters more than many borrowers realize.

The repayment term is the time you have to pay back the loan. Common personal loan terms vary by lender, and the term can affect both the monthly payment and total cost.

A longer term may make the loan appear more affordable because the monthly payment is lower. However, the total cost can be higher if interest builds over a longer period.

A shorter term may feel less comfortable month to month, but it may reduce the total interest paid.

When comparing terms, ask yourself:

- Can I afford the monthly payment without stretching my budget?

- How much will I repay in total?

- Is the lower payment worth the longer repayment period?

- Would a shorter term save money?

- Do I expect my income or expenses to change during the loan term?

A personal loan should not only be affordable today. It should also be realistic for the full repayment period.

Fixed Rates Are Usually Easier to Budget Around

Fixed interest rates are common for personal loans. A fixed rate means the interest rate stays the same during the repayment term. In most cases, that also means your monthly payment stays the same.

This can make budgeting easier. You know what is due each month, and you can plan around the payment.

Some loans may come with variable rates. A variable rate can change over time. If the rate increases, your cost may rise. If the rate decreases, your cost may fall. Variable rates may look appealing at first, but they add uncertainty.

For many borrowers, especially those trying to keep a stable monthly budget, a fixed-rate personal loan is easier to understand and compare.

Before accepting any offer, confirm whether the rate is fixed or variable. Do not assume the payment will stay the same unless the loan terms clearly say so.

Fees Can Change the Real Cost of the Loan

Fees can make a big difference.

Some personal loans come with origination fees. This is a fee charged for processing the loan. A lender may deduct the fee from the loan amount before sending you the funds, or it may include the fee in the loan cost.

For example, if a lender deducts an origination fee, the amount you receive may be less than the amount you borrowed. That matters if you need a specific amount of cash.

Other possible fees may include:

- Late payment fees

- Returned payment fees

- Administrative fees

- Application fees

- Prepayment penalties

Not every lender charges the same fees. Some lenders may advertise no origination fees, while others may charge them depending on the applicant or loan type.

Review the fees carefully before choosing a loan. Sometimes, a loan with a higher APR but lower fees can make more sense than a loan with a lower advertised rate and significant upfront costs.

Check Whether Early Payoff Costs Extra

Some borrowers want the option to pay off a loan early. Maybe they expect a tax refund, bonus, commission, or another source of cash later. Paying off a loan early can reduce interest costs, but only if the lender allows it without extra charges.

A prepayment penalty is a fee charged when you pay off a loan earlier than scheduled. Not all lenders charge this fee, but it is worth checking.

Before accepting a loan, look for answers to these questions:

- Can I make extra payments?

- Will extra payments reduce the principal balance?

- Is there a prepayment penalty?

- Are there any restrictions on paying off the loan early?

If you think you may repay the loan ahead of schedule, this part of the agreement matters. A loan with no prepayment penalty may give you more flexibility.

Do Not Borrow More Than You Need

Accepting a larger loan can be tempting when a lender offers it. But a larger loan also means a larger balance, more interest, and a longer repayment commitment.

Before you apply, decide how much you actually need to borrow.

If you are using the loan for a specific expense, calculate the amount carefully. If there are fees, consider whether the amount you receive after fees will still cover the expense. Avoid borrowing extra money simply because it is available.

A personal loan is not free money. Every dollar borrowed has to be repaid, usually with interest.

Review Eligibility Before You Apply

Every lender has its own approval process. Some lenders focus heavily on credit score. Others may also consider income, employment, banking history, debt-to-income ratio, or other factors.

Common eligibility factors may include:

- Credit history

- Income

- Employment status

- Existing debt

- Debt-to-income ratio

- State of residence

- Bank account information

- Loan amount requested

Meeting basic requirements does not guarantee approval. It only means you may be eligible to apply.

If a lender offers prequalification with a soft credit check, that may help you review possible rates without a hard inquiry. Always confirm how the lender handles credit checks before submitting information.

Compare More Than One Offer When Possible

If you only look at one lender, you may not know whether the offer is competitive. Comparing multiple options can give you a better sense of what rates, terms, and fees are available for your situation.

Compare each offer using the same details:

- Loan amount

- APR

- Monthly payment

- Repayment term

- Fees

- Funding speed

- Fixed or variable rate

- Prepayment rules

- Total repayment amount

Try to compare loans side by side. A simple table or checklist can make the differences easier to see.

A Simple Personal Loan Comparison Checklist

Before accepting a personal loan offer, review these questions:

- Is the loan secured or unsecured?

- What is the APR?

- Is the rate fixed or variable?

- What is the monthly payment?

- What is the repayment term?

- Are there origination fees?

- Are there late fees or returned payment fees?

- Is there a prepayment penalty?

- How much will you repay in total?

- Does the payment fit your monthly budget?

If any part of the loan terms is unclear, do not rush. Read the agreement and ask questions before moving forward.

Before You Apply

Before you accept a personal loan offer, review the APR, fees, repayment term, monthly payment, and total repayment amount. Make sure the payment fits your budget and that you understand any fees, collateral requirements, or early payoff rules.

Learning how to compare personal loan offers is mostly about looking at the full cost, not just the payment a lender advertises.

If you are still deciding whether a loan is right for you, read our guide on how to choose a personal loan before applying.

The Consumer Financial Protection Bureau explains that APR includes the interest rate plus certain additional loan costs, which makes it useful when comparing loan offers.

The Federal Trade Commission warns borrowers to be careful with lenders that ask for upfront fees before providing a loan.

{kind=link}